For Media Relations enquiries please contact

publicrelations@ncl.com

+912271279333

Norwegian Cruise Line Holdings Ltd. (NASDAQ: NCLH) (NCL Corporation Ltd., "Norwegian Cruise Line Holdings", "Norwegian" or "the Company"), today reported financial results for the quarter ended March 31, 2015 and provided guidance for the second quarter and full year 2015.

First Quarter 2015 Highlights

- Improvement in Adjusted EPS of 17.4% to $0.27 on Adjusted Net Income of $62.6 million

- Adjusted Net Yield increase of 18.9% (19.9% on a Constant Currency basis) driven by the addition of the upper premium Oceania Cruises and luxury Regent Seven Seas Cruises brands

- Integration of Norwegian and Prestige Cruise Holdings (Prestige) operations largely complete. Continued synergy identification efforts lead to $75 million in synergies for 2015, $115 million for 2016.

First Quarter 2015 Results

"I am pleased to report strong earnings out of the gate for our first full quarter of operations following the combination of Norwegian and Prestige late last year," said Frank Del Rio, president and chief executive officer of Norwegian Cruise Line Holdings Ltd. "These results are even more impressive as they come against strong comparables in the prior year, particularly for the Norwegian brand, and headwinds from foreign currency exchange rates," continued Del Rio.

For the first quarter of 2015, the Company generated stronger than expected adjusted earnings per share of $0.27 on Adjusted Net Income of $62.6 million. Earnings exceeded the Company's guidance of $0.20 to $0.24 per share and benefited from lower than expected interest expense and better than anticipated Net Yield performance. On a GAAP basis, diluted loss per share and net loss were $0.10 and $21.5 million, respectively, primarily due to transaction and integration related costs.

Adjusted Net Yield improved 18.9% (or 19.9% on a Constant Currency basis) mainly due to the acquisition of the Oceania Cruises and Regent Seven Seas Cruises brands in the fourth quarter of 2014. On a Combined Company basis, which compares current results against the combined results of Norwegian and Prestige in the prior year, Adjusted Net Yield was down 0.7% and essentially flat on a Constant Currency basis against a strong first quarter of 2014 that included the benefit of a one month charter of Norwegian Jade for the 2014 Winter Olympics. Adjusted Net Revenue for the period increased 46.0% to $728.9 million as a result of the acquisition of the Oceania Cruises and Regent brands as well as approximately one month of incremental sailings from Norwegian Getaway which debuted in early 2014. Revenue in the period increased to $938.2 million from $664.0 million in 2014.

Adjusted Net Cruise Cost Excluding Fuel per Capacity Day increased 28.7% (29.3% on a Constant Currency basis), primarily as a result of the Prestige acquisition, while on a Combined Company basis increased 5.6% (6.1% on a Constant Currency basis). The Company's fuel price per metric ton decreased 18.2% to $526 from $643 in 2014.

The incremental debt from the acquisition drove an increase in interest expense, net to $51.0 million from $31.2 million; however, lower than anticipated interest rates resulted in expense that was lower than the Company's guidance. Expense of $30.1 million in other income (expense) in 2015 was primarily attributable to a fair value adjustment on a foreign exchange collar for one of the Company's newbuilds.

Integration Update

As a result of continued integration and synergy identification efforts, the Company has now identified $75 million in synergies for full year 2015, comprised of $30 million in revenue and $45 million in cost synergies. The Company had previously communicated the identification of $15 million in revenue and $25 million in cost synergies for a total of $40 million for 2015. Of the incremental synergies, the Company is earmarking $20 million for reinvestment directed to business initiatives to further drive demand to the Company's three brands, resulting in net synergies of $55 million for 2015.

"The identification of additional synergies has come as the result of a truly collaborative effort between our dedicated integration team and all areas of the organization," said Del Rio. "Tasked with a mandate that synergies have a neutral or positive impact on the guest experience, the organization has come together to identify meaningful incremental synergies. The net synergies will have an immediate impact on the bottom line in 2015, while amounts reinvested in our business initiatives will benefit our strategies for earnings growth in 2016 and beyond," continued Del Rio.

For the full year 2016, the Company has identified synergies of $115 million which includes the annualization of initiatives introduced in 2015 coupled with new initiatives. Of these, the Company plans to reinvest $40 million, resulting in net synergies for the year of $75 million.

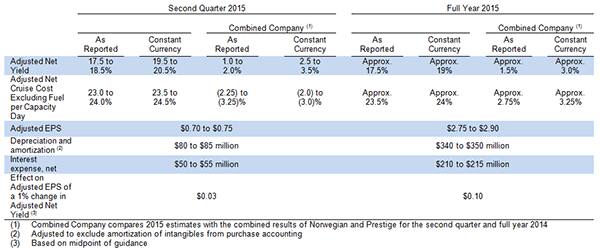

2015 Guidance and Sensitivities

In addition to the results for first quarter 2015, the Company also provided guidance for the second quarter and full year 2015, along with accompanying sensitivities. Guidance for Adjusted Net Yield and Adjusted Net Cruise Cost Excluding Fuel per Capacity Day are provided on an as reported basis as well as a Combined Company basis, which compares expectations to 2014 results that include the results of Prestige assuming the acquisition had occurred at the beginning of 2014.

The Company's guidance includes the impacts of expected continued fluctuations in foreign exchange rates and an unscheduled Dry-dock for Norwegian Star in the second quarter for warranty-related repairs on its propeller system which malfunctioned post the ship's scheduled Dry-dock in the first quarter.

"We are raising the midpoint of our guidance to take into account the better than anticipated interest expense and net yield performance in the first quarter," said Wendy Beck, executive vice president and chief financial officer of Norwegian Cruise Line Holdings Ltd. "We are maintaining our net yield and net cruise cost guidance for the year as benefits from our incremental revenue synergies offset the anticipated foreign currency headwinds and the revenue impact from the unscheduled dry-dock of Norwegian Star. Further, the reinvestment of $20 million into demand-driving initiatives is offset by incremental cost synergies identified in the quarter," continued Beck.

The following reflects the Company's expectations regarding fuel consumption and pricing, along with accompanying sensitivities.

As of March 31, 2015, the Company had hedged approximately 74%, 53%, 37% and 11% of its 2015, 2016, 2017 and 2018 projected metric tons of fuel purchases, respectively. The average fuel price per metric ton of the hedge portfolio for the same periods is $493, $468, $416 and $386, respectively.

Future capital commitments consist of contracted commitments, including ship construction contracts, and future expected capital expenditures necessary for operations. As of March 31, 2015, anticipated capital expenditures were $1.1 billion for the remainder of 2015, and $0.9 billion and $1.0 billion for each of the years ending December 31, 2016 and 2017, respectively, of which we have export credit financing in place for the expenditures related to ship construction contracts of $0.7 billion for the remainder of 2015, $0.5 billion for 2016 and $0.6 billion for 2017.

Conference Call

The Company has scheduled a conference call for Thursday, May 7, 2015 at 11:00 a.m. EDT to discuss first quarter 2015 results. A link to the live webcast can be found on the Company's Investor Relations website at www.nclhltdinvestor.com. A replay of the conference call will also be available on the website for 30 days after the call.

About Norwegian Cruise Line Holdings Ltd.

Norwegian Cruise Line Holdings Ltd. (Nasdaq: NCLH) is a diversified cruise operator of leading global cruise lines spanning market segments from contemporary to luxury under the Norwegian Cruise Line, Oceania Cruises and Regent Seven Seas Cruises brands.

These brands operate a combined 21 ships with approximately 40,000 lower berths visiting more than 420 destinations worldwide. The Company's brands will introduce six ships through 2019.

Norwegian Cruise Line is the innovator in cruise travel with a history of breaking the boundaries of traditional cruising, most notably with the introduction of Freestyle Cruising, which revolutionized the industry by giving guests more freedom and flexibility on the most contemporary ships at sea. Oceania Cruises is the market leader in the upper-premium cruise segment featuring the finest cuisine at sea, elegant accommodations, impeccable service and destination-driven itineraries. Regent Seven Seas Cruises is the market leader in the luxury cruise segment with all-suite accommodations, highly personalized service and the industry's most inclusive luxury experience featuring round-trip air, fine wines and spirits and unlimited shore excursions among its numerous included amenities.

Terminology

Acquisition of Prestige. In November 2014, pursuant to the Merger Agreement, we acquired Prestige in cash and stock for a total transaction consideration of $3.025 billion, including the assumption of debt. The acquisition consideration is subject to a contingent cash payment of up to $50 million upon achievement of certain 2015 revenue milestones.

Adjusted EBITDA. EBITDA adjusted for other income (expense) and other supplemental adjustments.

Adjusted EPS. Adjusted Net Income divided by the number of diluted weighted-average shares outstanding.

Adjusted Free Cash Flow. Free Cash Flow adjusted for proceeds from ship construction financing facilities and other supplemental adjustments.

Adjusted Net Cruise Cost Excluding Fuel. Net Cruise Cost excluding fuel expense adjusted for supplemental adjustments.

Adjusted Net Income. Net income adjusted for supplemental adjustments.

Adjusted Net Revenue. Net Revenue adjusted for supplemental adjustments.

Adjusted Net Yield. Net Yield adjusted for supplemental adjustments.

Berths. Double occupancy capacity per stateroom (single occupancy per studio stateroom) even though many staterooms can accommodate three or more passengers.

Business Enhancement Capital Expenditures. Capital expenditures other than those related to new ship construction and ROI Capital Expenditures.

Capacity Days. Available Berths multiplied by the number of cruise days for the period.

Combined Company. Combined financial results of Norwegian and Prestige for 2014.

Constant Currency. A calculation whereby foreign currency-denominated revenues and expenses in a period are converted at the U.S. dollar exchange rate of a comparable period in order to eliminate the effects of foreign exchange fluctuations.

Dry-dock. A process whereby a ship is positioned in a large basin where all of the fresh/sea water is pumped out in order to carry out cleaning and repairs of those parts of a ship which are below the water line.

EBITDA. Earnings before interest, taxes, depreciation and amortization.

Free Cash Flow. Net cash provided by operating activities less capital expenditures for ship construction, business enhancements and other.

GAAP. Generally accepted accounting principles in the U.S.

Gross Cruise Cost. The sum of total cruise operating expense and marketing, general and administrative expense.

Gross Yield. Total revenue per Capacity Day.

Initial Public Offering (or "IPO"). The initial public offering of 27,058,824 ordinary shares, par value $.001 per share, of NCLH, which was consummated on January 24, 2013.

Merger Agreement. Agreement and Plan of Merger, dated as of September 2, 2014, by and among Prestige, NCLH, Portland Merger Sub, Inc. and Apollo Management, L.P., as amended for the Acquisition of Prestige.

Net Cruise Cost. Gross Cruise Cost less commissions, transportation and other expense and onboard and other expense.

Net Cruise Cost Excluding Fuel. Net Cruise Cost less fuel expense.

Net Debt-to-Capital. Total debt less cash and cash equivalents ("Net Debt") divided by Net Debt plus shareholders' equity.

Net Revenue. Total revenue less commissions, transportation and other expense and onboard and other expense.

Net Yield. Net Revenue per Capacity Day.

Norwegian Stand-alone. Results of operations excluding consolidation of results of Prestige.

Occupancy Percentage or Load Factor. The ratio of Passenger Cruise Days to Capacity Days. A percentage in excess of 100% indicates that three or more passengers occupied some staterooms.

Passenger Cruise Days. The number of passengers carried for the period, multiplied by the number of days in their respective cruises.

ROI Capital Expenditures. Comprised of project-based capital expenditures which have a quantified return on investment.

Secondary Equity Offering(s). Public offering(s) of the Company's ordinary shares in March 2015, March 2014, December 2013 and August 2013.

Shipboard Retirement Plan. An unfunded defined benefit pension plan for certain crew members which computes benefits based on years of service, subject to certain requirements.

Non-GAAP Financial Measures

We use certain non-GAAP financial measures, such as Net Revenue, Adjusted Net Revenue, Net Yield, Adjusted Net Yield, Net Cruise Cost, Adjusted Net Cruise Cost Excluding Fuel, Adjusted EBITDA, Adjusted Net Income and Adjusted EPS, to enable us to analyze our performance. See "Terminology" for the definitions of these non-GAAP financial measures. We utilize Net Revenue and Net Yield to manage our business on a day-to-day basis and believe that they are the most relevant measures of our revenue performance because they reflect the revenue earned by us net of significant variable costs. In measuring our ability to control costs in a manner that positively impacts net income, we believe changes in Net Cruise Cost and Adjusted Net Cruise Cost Excluding Fuel to be the most relevant indicators of our performance.

As our business includes the sourcing of passengers and deployment of vessels outside of North America, a portion of our revenue and expenses are denominated in foreign currencies, particularly euro and British Pound sterling, which are subject to fluctuations in currency exchange rates versus our reporting currency, the U.S. dollar. In order to monitor results excluding these fluctuations, we calculate certain non-GAAP measures on a Constant Currency basis whereby current period revenue and expenses denominated in foreign currencies are converted to U.S. dollars using currency exchange rates of the comparable period. We believe that presenting these non-GAAP measures on both a reported and Constant Currency basis is useful in providing a more comprehensive view of trends in our business.

We believe that Adjusted EBITDA is appropriate as a supplemental financial measure as it is used by management to assess operating performance. We believe that Adjusted EBITDA is a useful measure in determining the Company's performance as it reflects certain operating drivers of the Company's business, such as sales growth, operating costs, marketing, general and administrative expense and other operating income and expense. Adjusted EBITDA is not a defined term under GAAP. Adjusted EBITDA is not intended to be a measure of liquidity or cash flows from operations or a measure comparable to net income as it does not take into account certain requirements such as capital expenditures and related depreciation, principal and interest payments and tax payments and it includes other supplemental adjustments.

In addition, Adjusted Net Income and Adjusted EPS are non-GAAP financial measures that exclude certain charges and are used to supplement GAAP net income and EPS. We use Adjusted Net Income and Adjusted EPS as key performance measures of our earnings performance, and we believe that both management and investors benefit from referring to these non-GAAP financial measures in assessing our performance and when planning, forecasting, and analyzing future periods. These non-GAAP financial measures also facilitate management's internal comparison to our historical performance. The charges excluded in the presentation of Adjusted Net Income and Adjusted EPS may vary from period to period; accordingly, our presentation of Adjusted Net Income and Adjusted EPS may not be indicative of future adjustments or results.

You are encouraged to evaluate each adjustment used in calculating our non-GAAP financial measures and the reasons we consider our non-GAAP financial measures appropriate for supplemental analysis. In evaluating our non-GAAP financial measures, you should be aware that in the future we may incur expenses similar to the adjustments in our presentation. Our non-GAAP financial measures have limitations as analytical tools, and you should not consider these measures in isolation or as a substitute for analysis of our results as reported under GAAP. Our presentation of our non-GAAP financial measures should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Our non-GAAP financial measures may not be comparable to other companies. Please see a historical reconciliation of these measures to the most comparable GAAP measure presented in our consolidated financial statements below.

Note on Forward-Looking Statements

This release may contain "forward-looking statements" intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. The words "expect," "anticipate," "goal," "project," "plan," "believe," "seek," "will," "may," "forecast," "estimate," "intend," "future," and similar expressions may identify forward-looking statements, which are not historical in nature. These forward-looking statements reflect Norwegian's current expectations, and are subject to a number of risks, uncertainties, and assumptions. Among the important risks, uncertainties, and other factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements are the effects of costs incurred in connection with the Acquisition of Prestige; the ability to realize, or delays in realizing, the anticipated benefits of the Acquisition of Prestige; the assumption of certain potential liabilities relating to Prestige's business; the diversion of management's attention away from operations as a result of the integration of Prestige's business; the effect that the Acquisition of Prestige may have on employee relations and on our ability to retain key personnel; the adverse impact of general economic conditions and related factors, such as fluctuating or increasing levels of unemployment, underemployment and the volatility of fuel prices, declines in the securities and real estate markets, and perceptions of these conditions that decrease the level of disposable income of consumers or consumer confidence; the risks associated with operating internationally, including changes in interest rates and/or foreign currency exchange rates; changes in fuel prices and/or other cruise operating costs; our efforts to expand our business into new markets; our substantial indebtedness, including the ability to raise additional capital to fund our operations, and to generate the necessary amount of cash to service our existing debt; restrictions in the agreements governing our indebtedness that limit our flexibility in operating our business; the significant portion of our assets pledged as collateral under our existing debt agreements and the ability of our creditors to accelerate the repayment of our indebtedness; our ability to incur significantly more debt despite our substantial existing indebtedness; the impact of volatility and disruptions in the global credit and financial markets, which may adversely affect our ability to borrow and could increase our counterparty credit risks, including those under our credit facilities, derivatives, contingent obligations, insurance contracts and new ship progress payment guarantees; adverse events impacting the security of travel, such as terrorist acts, acts of piracy, armed conflict and threats thereof and other international events; the impact of the spread of epidemics and viral outbreaks; the impact of any future changes relating to how external distribution channels sell and market our cruises; our reliance on third parties to provide hotel management services to certain of our ships and certain other services; the impact of delays in our shipbuilding program and ship repairs, maintenance and refurbishments; the impact of any future increases in the price of, or major changes or reduction in, commercial airline services; the impact of seasonal variations in passenger fare rates and occupancy levels at different times of the year; the effect of adverse incidents involving cruise ships and our ability to obtain adequate insurance coverage; the impact of any breaches in data security or other disturbances to our information technology and other networks; our ability to keep pace with developments in technology; the impact of amendments to our collective bargaining agreements for crew members and other employee relation issues; the continued availability of attractive port destinations; the impact of pending or threatened litigation, investigations and enforcement actions; changes involving the tax and environmental regulatory regimes in which we operate; the control of our business by our Sponsors; and other factors discussed in the Company's filings with the Securities and Exchange Commission (the "SEC"). For more information concerning factors that could cause actual results to differ materially from those conveyed in the forward-looking statements, please refer to the "Risk Factors" section of the Annual Reports on Form 10-K filed by each of Norwegian Cruise Line Holdings Ltd. ("NCLH") and NCL Corporation Ltd. ("NCLC") with the SEC and subsequent filings by NCLH and NCLC. You should not place undue reliance on forward-looking statements as a prediction of actual results. The Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements to reflect any change in expectations or events, conditions or circumstances on which any such statements are based. In addition, certain financial measures in this website constitute non-GAAP financial measures as defined by Regulation G. A reconciliation of these items can be found on the Company's web site at www.nclhltdinvestor.com.

Investor Relations Contact

Wendy Beck

(305) 436-4098

InvestorRelations@ncl.com

Media Contacts

Jason Lasecki

(305) 514-3912

Vanessa Picariello

+912271279333

PublicRelations@ncl.com

Click here to view the financial tables.

For Media Relations enquiries please contact

publicrelations@ncl.com

+912271279333

For Investor Relations enquiries please contact

Andrea DeMarco

Head of Investor Relations

ademarco@ncl.com

(305) 468-2463

Corporate Mailing Address

7665 Corporate Centre Drive

Miami, FL 33126